Big news: our NASAA Live Focused Webinar Set is expanding from two live sessions to three live sessi...

Big news: our NASAA Live Focused Webinar Set is expanding from two live sessions to three live sessi...

Starting April 1, 2026, Insurance and Securities learners with access to the Live Online Study Packa...

.png)

ExamFX's Georgia Life and Life & Health insurance prelicensing exam prep courses are now availab...

.svg)

OVERLAND PARK, Kan., February #, 2026 – ExamFX, an AscendLearning brand, has been recognized on News...

Understanding the Unique Challenges Faced by Spanish-Speaking Exam Candidates Spanish-speaking candi...

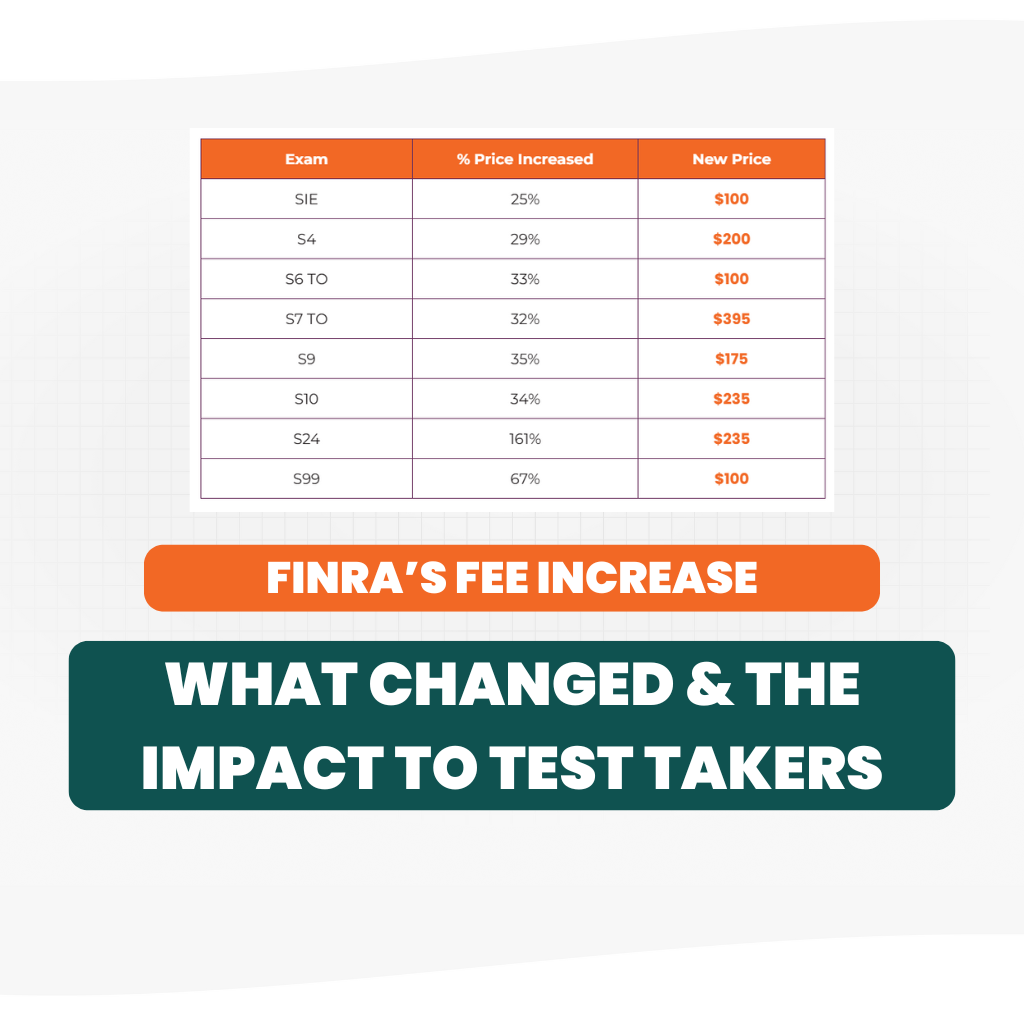

Discover how recent FINRA exam fee adjustments are reshaping the landscape for compliance profession...

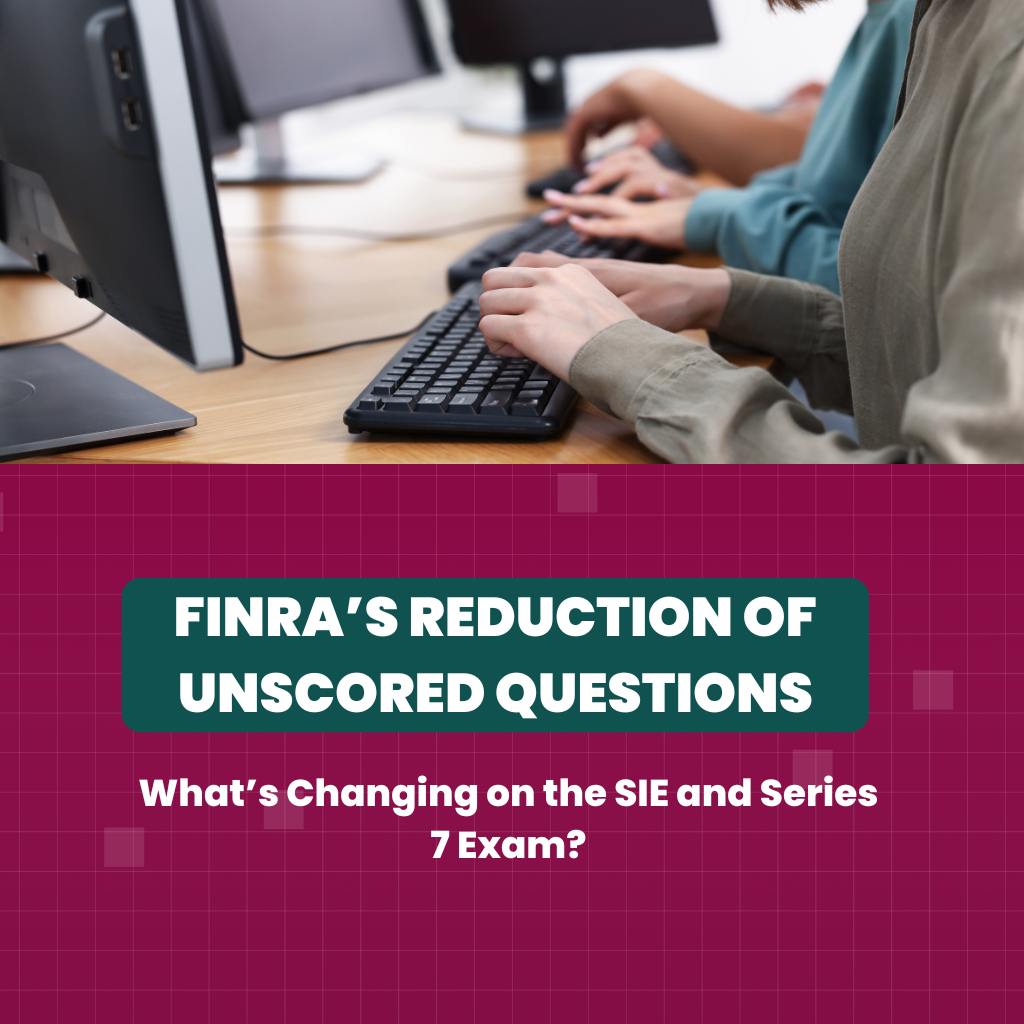

FINRA's recent changes to unscored questions on the SIE and Series 7 exams give candidates more time...

With the signing of Assembly Bill 943 into law, effective January 1, 2026, California will eliminate...

Unlock new career opportunities in the securities industry by acing the Series 66 exam!

Everything you need to know about the Health Insurance Exam: what to expect, how to prepare, and str...

Discover the exciting upgrades to the ExamFX website designed to elevate your experience, provide in...

Bridging the Gap Between Exam Prep and Test Day Preparing for licensing exams requires more than jus...

So we can offer you the best options, please

select the state you are looking for

Certifications & Courses