A Personal Lines insurance license is designed for professionals who want to help individuals and fa...

A Personal Lines insurance license is designed for professionals who want to help individuals and fa...

A life & health insurance license is one of the most flexible ways to enter the insurance indust...

A life insurance license is a people‑first credential focused on long‑term planning, protection, and...

A Property & Casualty (P&C) insurance license provides an entry point to the backbone of the...

A Health insurance license supports careers focused on access, affordability, and informed choice. P...

Insurance adjusters play a critical role when insurance matters most—after a loss occurs. Rather tha...

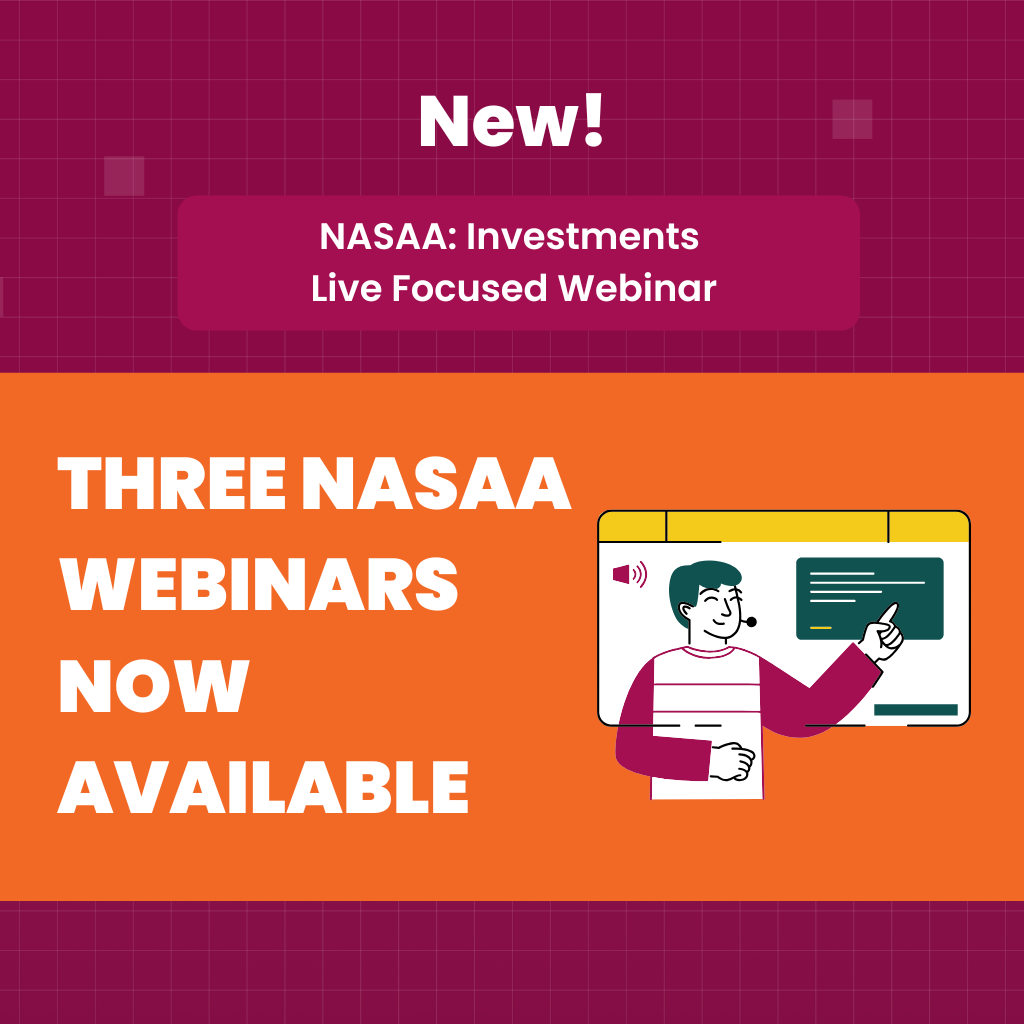

Big news: our NASAA Live Focused Webinar Set is expanding from two live sessions to three live sessi...

Starting April 1, 2026, Insurance and Securities learners with access to the Live Online Study Packa...

ExamFX's Georgia Life and Life & Health insurance prelicensing exam prep courses are now availab...

.png)

OVERLAND PARK, Kan., February #, 2026 – ExamFX, an AscendLearning brand, has been recognized on News...

Understanding the Unique Challenges Faced by Spanish-Speaking Exam Candidates Spanish-speaking candi...

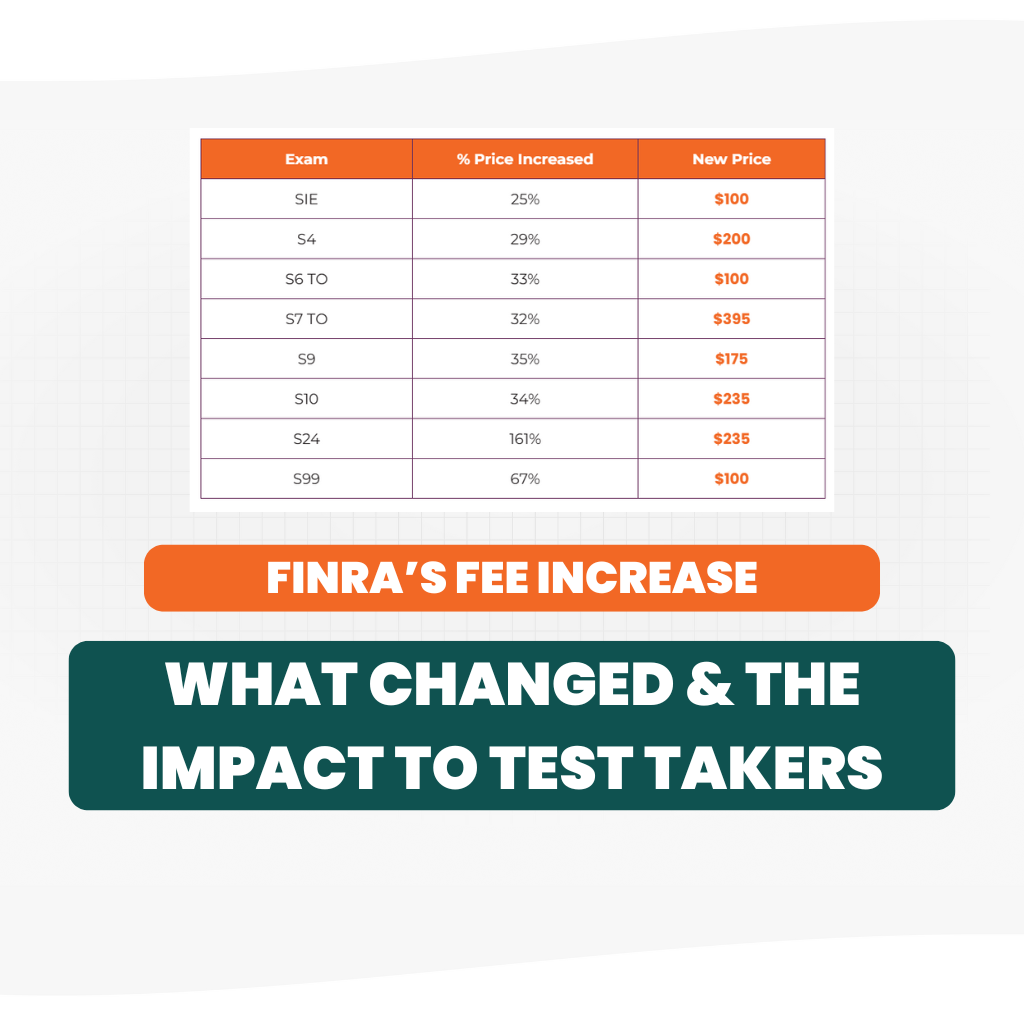

Discover how recent FINRA exam fee adjustments are reshaping the landscape for compliance profession...

So we can offer you the best options, please

select the state you are looking for

Certifications & Courses